Black Scholes Model for Option Pricing - Interview Questions 🚀🚀

Webiste: www.qfeuniversity.com

Basic Concepts and Assumptions 😄😄

1. What is the Black-Scholes model?

2. Who were the creators of the Black-Scholes model?

3. What is the main purpose of the Black-Scholes model?

4. What types of options can be priced using the Black-Scholes model?

5. What are the key assumptions of the Black-Scholes model?

6. Explain the concept of risk-neutral pricing in the context of the Black-Scholes model.

7. How does the Black-Scholes model assume that stock prices behave?

8. What is the role of the volatility parameter in the Black-Scholes formula?

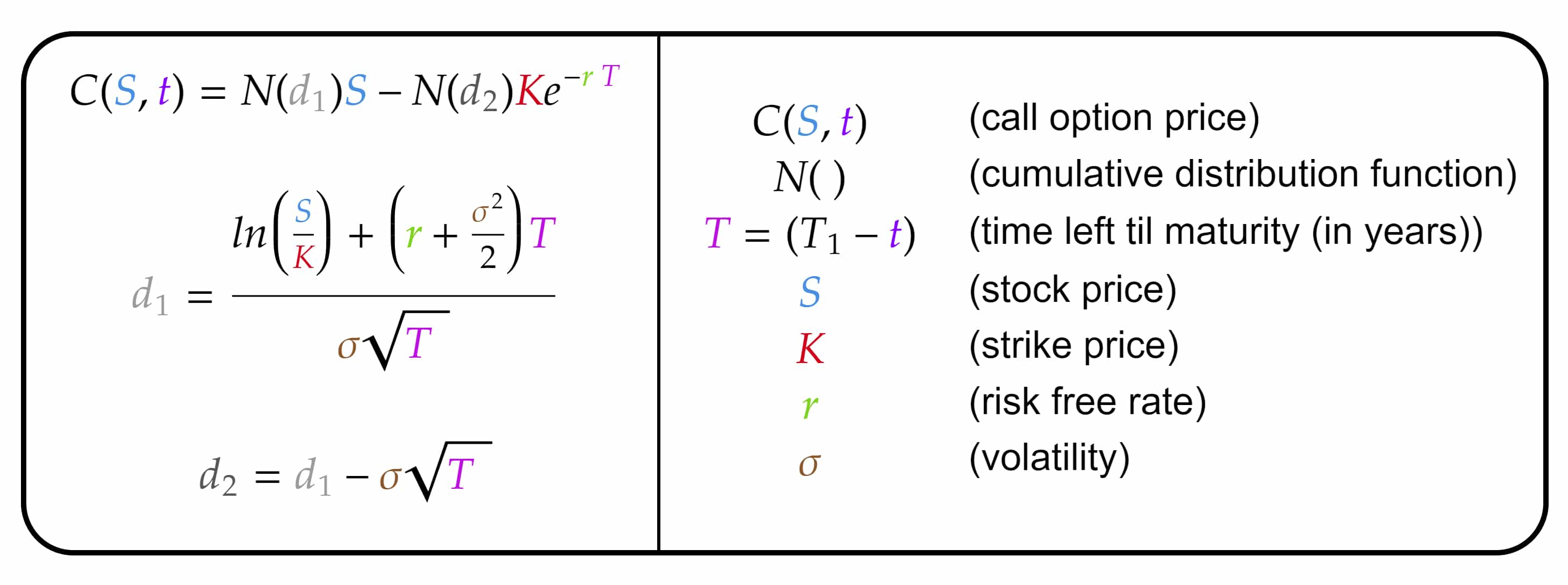

Option Pricing Formula and Parameters: 📚📚

9. Provide the formula for the Black-Scholes option pricing model.

10. What do each of the variables in the Black-Scholes formula represent?

11. Explain the significance of the term "d1" and "d2" in the formula.

12. How does the strike price affect the value of an option according to the Black-Scholes model?

13. How does the time to expiration influence the option's value in the Black-Scholes model?

14. What is the relationship between volatility and option prices in the Black-Scholes model?

15. How does an increase in the risk-free interest rate impact option prices in the Black-Scholes model?

16. What is the connection between the price of the underlying asset and the value of a call or put option?

Limitations and Extensions: 😀😀

17 Discuss some limitations of the Black-Scholes model.

18 How does the Black-Scholes model handle dividends?

19 Can the Black-Scholes model be applied to options on stocks that do not pay dividends?

20 What is the concept of implied volatility, and how does it relate to the Black-Scholes model?

21 Are there any alternative models to the Black-Scholes model for option pricing?

22. What is the Merton Jump-Diffusion Model, and how does it address a limitation of the Black-Scholes model?

Volatility and Option Greeks: 📕

23. Explain the concept of "volatility smile" or "volatility skew."

24. How can the Black-Scholes model be adjusted to account for a volatility smile?

25. Define Delta, Gamma, Vega, Theta, and Rho. How are these Greeks calculated using the Black-Scholes model?

26. How does Delta represent the sensitivity of option price to changes in the underlying asset's price?

27. What is Gamma, and why is it important for option traders?

28. What does Vega measure, and how does it impact option prices?

Applications and Practical Use:

29. In what situations is the Black-Scholes model most suitable for pricing options?

30. How can option traders use the Black-Scholes model to make informed trading decisions?

31. What role does the Black-Scholes model play in risk management for financial institutions?

32. Explain how the Black-Scholes model can be used for option valuation in mergers and acquisitions.

33. How does the Black-Scholes model impact the pricing of exchange-traded options?

#financialengineering #blackschole #optionpricing #quantfinance #interviewquestion